Three game-changing ways embedded finance is boosting SMB growth in Asia Pacific

In today's rapidly evolving digital economy, embedded finance is emerging as a transformative force, particularly for small and medium-sized businesses (SMBs) in the Asia Pacific region. By 2025, this innovative approach is expected to unlock a staggering over USD242 billion opportunity, with the majority of the value coming from SMBs.¹

Embedded finance integrates financial services directly into non-financial platforms. This provides SMBs, especially those outside the financial sector, with unprecedented access to essential financial tools. Integrating financial services not only enhances SMBs’ agility but also enables them to streamline operations, improve consumer experiences, and drive growth.

Recent developments in embedded payments, insurance, and lending are opening new avenues for SMBs to thrive, allowing them to meet diverse consumer needs without the burden of managing complex financial services infrastructures. As embedded finance continues to develop, it holds the potential to redefine the agility and success of SMBs across the region.

Embedded payments: Enhancing operational efficiency and financial accessibility

Embedded payment tools are transforming the financial operations of SMBs by integrating payment processes directly into existing business platforms. This integration streamlines financial operations, automating tasks such as invoicing and payment collection, which reduces complexity and minimises errors. These tools also offer reduced transaction fees and more competitive pricing structures compared to traditional payment systems. Moreover, embedded payment solutions improve cash flow management by providing real-time visibility into expenses and financial reports, enabling better decision-making. Advanced cash flow forecasting capabilities allow businesses to anticipate financial needs and manage liquidity effectively.

A recent innovation in embedded finance is the partnership between Visa, SAP, and Taulia.² Through integration, Visa’s APIs will embed virtual payment credentials, acceptance and enablement solutions directly into SAP business applications. The collaborative solution will allow CFOs, procurement teams, and accounts payable departments to automate payments to suppliers. The solution is particularly beneficial for one-time supplier payments, eliminating the need to create full master data in the system, which can typically take weeks or months.

Embedded lending: Empowering SMBs with better credit access and flexible payments

Another development is embedded lending which is transforming credit access for SMBs. By integrating lending services directly into the platforms SMBs use, embedded lending eliminates the need for navigating multiple websites or completing separate applications, creating a frictionless lending experience. For example, leading e-commerce platforms now offer loans to SMBs for financing inventory and marketing expenses, streamlining the purchasing process and enhancing operational efficiency.

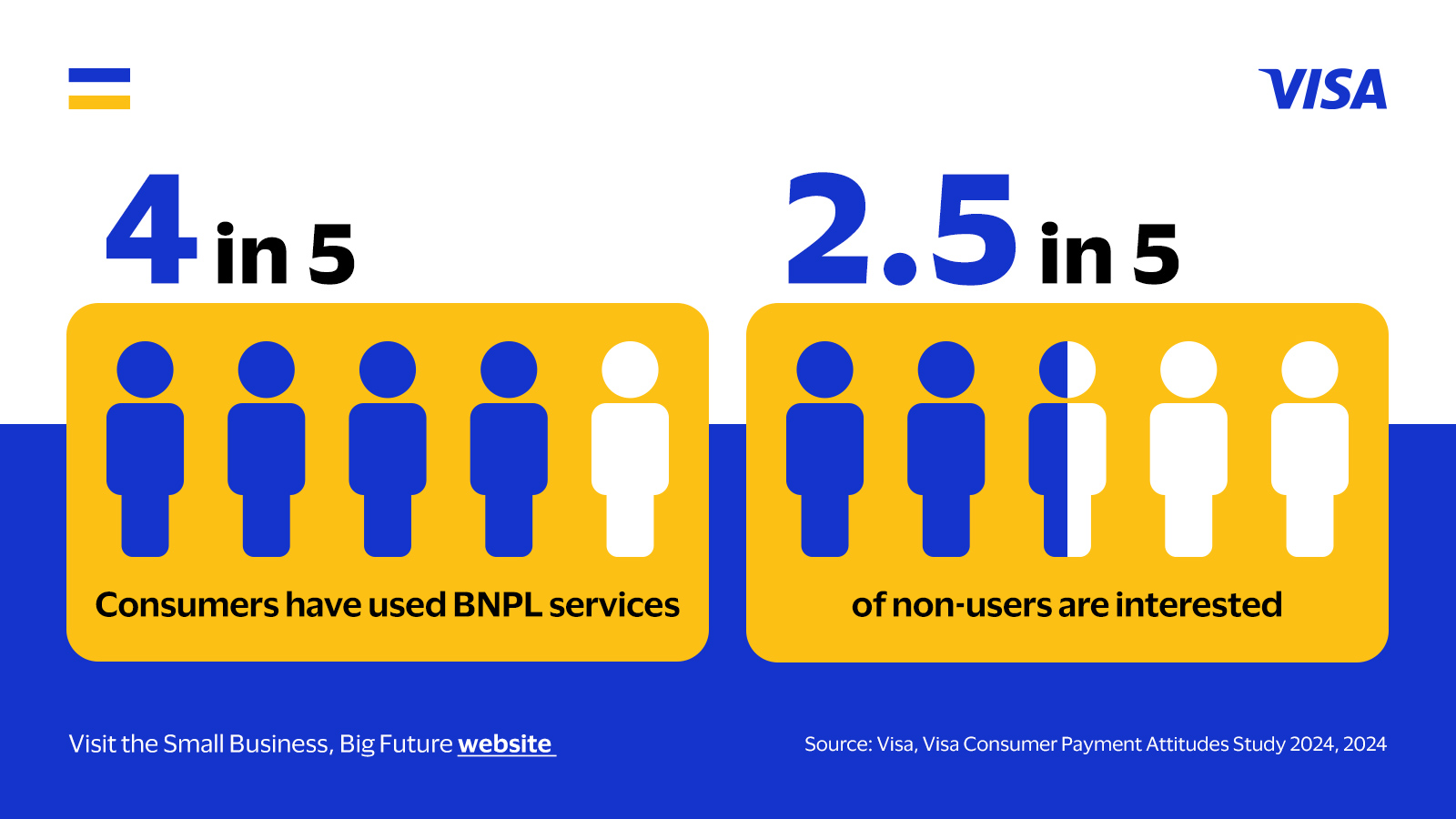

Additionally, embedded lending improves financial inclusion by making credit accessible to underserved segments, including SMBs that struggle with traditional bank loans and consumers with limited credit histories. By broadening access to financial services, embedded lending opens new growth opportunities. SMBs can use these features, such as Buy Now Pay Later (BNPL) services, on digital platforms to make buying easier for consumers. BNPL—used by 85 per cent of Southeast Asian consumers—match payment methods with what buyers prefer, helping to boost sales.³

Embedded insurance: Tailoring consumer experiences and capturing future growth

Embedded insurance is another growing trend within embedded finance. It is transforming how SMBs enhance consumer experiences by providing personalised coverage options directly at the point of sale. This integration simplifies the process, allowing consumers to obtain relevant protection aligned with their specific purchases, which boosts satisfaction and adds value. For example, consumers have the ability to purchase insurance as part of their everyday transactions without having to switch apps or platforms, such as adding travel insurance when booking a flight or getting car insurance when renting a vehicle. By leveraging these value-added features through digital platforms, SMBs get to generate new revenue opportunities by offering personalised services that differentiate them.

Looking ahead, embedded insurance has significant growth potential as consumers increasingly seek personalised services. With 54 per cent of non-users in Southeast Asia interested in trying these products, SMBs can capitalise on this curiosity by offering customised coverage at the right moment.⁴ By embracing embedded insurance, SMBs can meet emerging consumer demands, attract new consumers, and drive long-term success in the evolving market.

Embedded finance offers a transformative opportunity for SMBs to enhance their agility by integrating financial services into non-financial platforms, particularly in payments, insurance, and lending. SMBs can take advantage of these services to meet diverse consumer needs, streamline operations, and improve financial accessibility.

As the landscape of embedded finance continues to evolve, there is significant potential for innovation, especially in the realm of embedded insurance. Fintechs, banks, and digital platforms are well-positioned to explore this space and deliver more personalised services that cater to the unique needs of SMBs and their consumers. Initiatives like the Visa Singapore Innovation Centre's focus on embedded finance underscore its potential to reshape financial services, enabling SMBs to thrive in an increasingly competitive market.⁵

¹ Visa, Empowering Agile SMBs through Innovation and Entrepreneurship, 2024.

² PYMNTS.com, Visa, Taulia Team on Embedded Finance as Credit Grows Scarce, 2024.

³ Visa, Visa Consumer Payment Attitudes Study 2024, 2024.

⁴ Visa, Visa Consumer Payment Attitudes Study 2024, 2024.

⁵ Visa, Visa Singapore Innovation Center ushers in a new era of payments, 2024.